Clearing Services

Since 2004, STET is one of the leading European Automated Clearing Houses (ACH), operating for the French and Belgian banking communities. STET clears and prepares payments of all types for settlement, including credit transfers, direct debits, cheques, cards, and other legacy payment means.

Authorization

Our secure payment and cash withdrawal authorization network operates 24/7 with very high resilience and 99.999% availability. It supports both French domestic scheme Cartes Bancaires and international card schemes (Visa, Mastercard…).

Digital Payments

Through STET Digital Solution (SDS), we enable banks to access tokens linked to digital cards via various wallets. It allows merchants to use tokenization services (e.g. Card on File).

Combined with the STET card authorization network, it offers a comprehensive coverage for all tokenized payment use cases, with the same guarantees as traditional card payments.

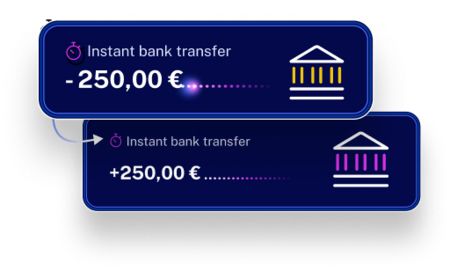

Instant Payments

STET has been delivering Instant Payment services to the French and Belgian banking communities since 2017. Our Instant Payment service complies with EPC requirements and offers European interoperability through interconnection with TIPS and RT1.

Fraud Prevention & Detection

STET’s fraud prevention and detection tools cover all payment means (cards, SEPA and digital wallets) and provide scoring across the entire payment process (authentication, enrolment, authorization, prepayment) using IA to continuously enhance our best-in-class fraud prevention solutions.

Secure Messaging

SEPAmail.eu, a STET subsidiary since 2024, is a market infrastructure provider that manages secure messaging schemes with a broad membership base defining a trust and security standard for digital data transfers and acting as a certification authority. SEPAmail.eu offers secure messaging services such as account switching and IBAN Name Check (Verification of Payee), and as such, serves as a routing and verification mechanism.