Doing more for banks today, and even more tomorrow

We assume our role with full dedication, encompassing day-to-day business operations and a long-term vision to anticipate the demands of tomorrow’s market.

As the European payments sector undergoes dramatic changes, arising from industry standardization, regulatory updates and technological upgrades, we remain dedicated to innovation. Our approach to continuous improvement drives us to design new, groundbreaking functional and technical solutions, underpinned by flexible architectures capable of adapting to future challenges.

Since its inception, STET vision has been that European harmonization should not impede market diversity. This is why we develop flexible and sustainable architectures designed to meet the varied needs of our clients through user-friendly, multi-channel services.

Innovating to anticipate the needs of the market

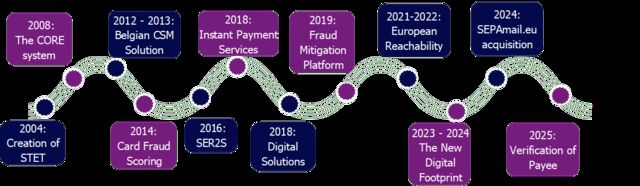

What is happening with the market? What will happen tomorrow and the next day/years? These questions are a major focus for us at STET.

At STET, we believe our primary mission is to serve our clients today and anticipate the expectations of tomorrow.

We closely monitor market developments to provide the best possible support to our clients and assist them as their needs evolve.

In the fast-changing technological landscape, we pay close attention to new technical developments and business trends in the market. As a technology service provider, we facilitate our clients’ transitions into the future and offer them new services that deliver time-to-market efficiency.

Governance

STET brings next-generation solutions with open access and clear user policies.

Our governance approach empowers each of our clients communities to maintain full control over their CSMs. This means that STET distinguishes clearly between the management of a CSM and the management of its scheme-agnostic processing capabilities. Each has its own governance organization, ensuring balanced priorities:

- The Board is responsible for managing the corporation. These responsibilities include overseeing STET’s corporate strategy, organization, investments, and future developments.

- For our Clearing services, a governing body is established for each community. The governance and structure of these bodies are determined by their communities which have full control over payment instruments and the rules for processing or routing them. Individual banks are also taken into consideration. Our flexible Clearing services allow clients to opt for additional services, such as Instant Payment.

- For our Card services, we have developed a flexible network of solutions that can be tailored to meet the evolving needs and requirements of the market.

A reliable partner of the European payments market

Our unique governance model, which engages all stakeholders and is supported by an open-access policy, enables all European banks to leverage our solid track record, robust system and network infrastructure, 24/7 processing capabilities and cost-efficient solutions.

Thanks to our clients continued support, we believe we are in a strong position to consolidate the European payments market from both a technical as well as business perspective.

Our comprehensive 360° service offering includes a Clearing system that can process a wide range of payment instruments, both domestic and SEPA, as well as a Routing and Authorization network. This ensures that we can support all means of payment.

Reachability is also a key issue for STET. This is why we are working on partnerships that will allow our clients to reach any counterpart within the SEPA area.

Finally, our clients enjoy our competitive pricing, which stems from optimized business processes and economies of scale generated by our large transaction volumes.